ETF Liquidity

ETF Liquidity

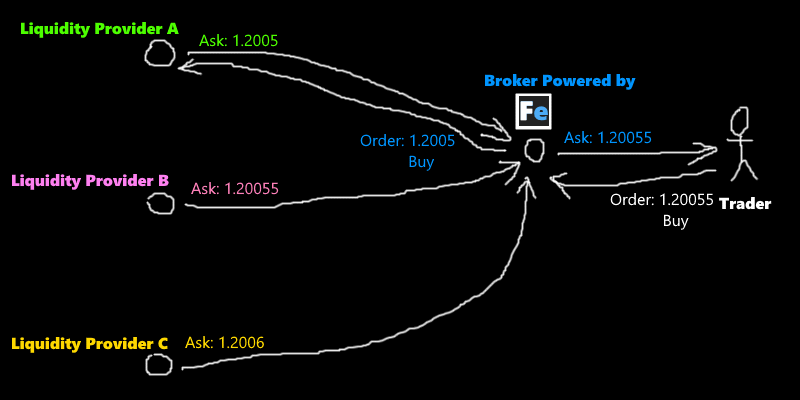

Fintechee provides cryptocurrency price on their website.

Here is the link: https://www.brokerless.cc, the frontend is based on Fintechee WEB Trader

AngelInvestmentNetwork.org has some cases.

We have these days been how spreads improve as price traded in a ticker improves.

Our latest archive reveals that however that style holds for ETFs, the fees of trading ETFs are much more affordable throughout the spectrum.

Cost traded is only one measure of liquidity. What we locate when we examine turnover might surprise you. Traders and merchants exhaust ETFs actual otherwise.

ETF spreads are an awful lot tighter than related spreads.

Once we evaluate spreads blueprint, vertical arbor in opposition to price traded horizontal arbor we discover a consistent downward diagonal form. This indicates that as liquidity improves, spreads get cheaper too.

Interestingly even though, after we examine ETFs pink dots to shares dejected dots youngsters the pattern is consistent, the spread costs for ETFs are almost always tremendously cheaper for the same stage of clamminess.

Blueprint: ETF spreads are normally enormously more affordable than stocks of related liquidity.

There are a number of factors for this, broadly speaking regarding the undeniable fact that ETFs also symbolize a portfolio of balance.

In the beginning, the ETF can customarily be arbitraged against the basal stocks. So ETF spreads compare stronger to the spreads of the underlying portfolio, which is always a great deal greater clamminess than the precise ETF ticker.

ETFs also have greater beta and less inventory certain risk, which makes them less complicated to hedge with futures or other ETFs. That, in turn, helps market makers preserve the rate of the ETF competitive.

Definitely, the clamminess that you just see “on the monitor,” representing the price that the ETF ticker trades, is nearly always an atom of the change dimension a liquidity provider may execute within the underlying portfolio. That makes it lots more affordable to assassinate significant trades in an ETF, however, the precise ETF ticker appears agilely traded.

ETF spreads are a good deal tighter for higher and greater liquid tickers.

Regardless of that, more clamminess nevertheless helps in the reduction of spreads. That’s partly as a result of aqueous ETF s commonly have natural ETF bids and offers that may have enough money to be greater aggressive than the expenses of the basal.

After we look in more element at ETFs chart and color by exposure and measurement by way of ETF belongings, we see every other trait too:

In normal, the greatest ETFs huge circles are also probably the most liquid added to the correct. however now not all the time. Some ETFs, like QQQs, EEM and sector SPDR’s accept turn into “futures like” as we discuss later.

Spreads are generally very low, % of all ETF tickers accept a selection internal foundation elements bps, apery % of all value traded. Despite ETF trading making up round % of all stock market value traded, most effective a scattering of ETF tickers exchange with enough liquidity to supply them spreads of lower than basis factor.

Handiest round a dozen tickers alternate greater than $ billion per day. spy dominates with clamminess of $ billion per day on assets of $ billion. That’s round thrice more aqueous than the most liquid corporates, although AMZN, AAPL, and MSFT all accept bazaar cap around several trillion.

Stock ETFs dejected dots are likely to accept tighter spreads than overseas stock ETFs green dots with identical liquidity. That’s probably reflective of the extra charges and risks ambiguity foreign inventory ETFs, where the underlying markets are often already bankrupt.

Although bond portfolios usually accept decrease animation, spreads on band ETFs orange circles are corresponding to spreads on U.S. inventory ETFs.

Apart from GLD the gold ETF, article ETFs red dots usually accept fairly added spreads. Be aware that many of these are based mostly on futures, which require rolls and margin, whereas many are structured as ETNs addendum as a substitute for mutual funds.

Chart: evaluating ETF clamminess, belongings and spreads colored by way of underlying exposures.

ETF liquidity is additionally actually targeted. simply tickers, or around 30% of all ETFs exchange greater per day. Despite the fact, this neighborhood provides to around $5 billion of daily trading cost or more than 85% of all ETF cost traded.

ETF turnover shows distinctive ETFs attract distinctive users.

However, value traded isn’t the most effective approach to examine liquidity.

We’ve previously looked at stocks buying and selling as a proportion of shares fabulous. We present in our appearance at the snake that the general significant cap inventory trades around their shares incredible each year. Thinly-traded stocks turned into much much less, but the smallest stocks basically had the highest turnover.

The same statistics for ETFs is a reasonably diverse chart:

Some ETFs exchange an awful lot although their assets are small excessive dots with small circle dimensions. Most of the ETFs with more than each year are levered or sector ETFs favorite with the aid of hedge cash and expert traders. These are almost all “boilerplate” index style portfolios.

In distinction, energetic, radiant beta and strategic ETF tickers chicken and red dots in blueprint have plenty lessen than regular stock.

According to these observations, it seems that barrier funds and expert traders exercise ETFs in different ways than many best-time period traders.

Those hunting for hedges or short-time period-appropriate exposures are understandably fatigued to the liquid and anticipated component exposures that many tremendous basis ETFs offer. With the aid of specializing in a few tickers, bazaar makers profit from economies of calibration, making spreads alike tighter. Many of these ETFs are utilized in identical methods to futures.

In the meantime, these buying ETFs with stock choice appear to be much greater interested in best-term investing. That’s also in line with a previous look at that found retail appear to dominate trading in smaller cap ETFs.

Chart three: comparing turnover

At the other end of the spectrum, the larboard aspect of that archive is a huge variety of agilely-traded ETFs.

The spread effects exhibit that agilely-traded ETFs don’t suffer from a scarcity of liquidity within the identical means that corporates do. Spreads are a great deal more cost-effective than agilely-traded corporates, even for ETFs that don’t trade daily.

However, ETFs with the bottom are also those with the aboriginal standard daily buying and selling, as well as customarily accepting a really baby asset despicable. There seems proof that actual low liquidity, which brings wider spreads, at last, asphyxiate trading absolutely, making it alike tougher to make these ETFs a success.

The information for ETFs is good. There s significant liquidity at very low priced spreads for these doing lots of buying and selling. There are also competitive spreads for greater mutual-armamentarium-like inventory selection ETFs that retail investors seem to more and more appreciated.